Making additional space in your home can be a perfect way of adding value, functionality, and comfort to your home. If you need a spare bedroom, a bigger kitchen, or a home office, a home addition can be a long-term investment that will pay off. But the cost of a home addition can be quite high, and financing such a project needs planning and consideration of all your options. In this guide, we will look at various means of financing a home addition such as loans, credit, and government programs to help you find the best option for your project.

Find Out the Scope and Cost of the Project

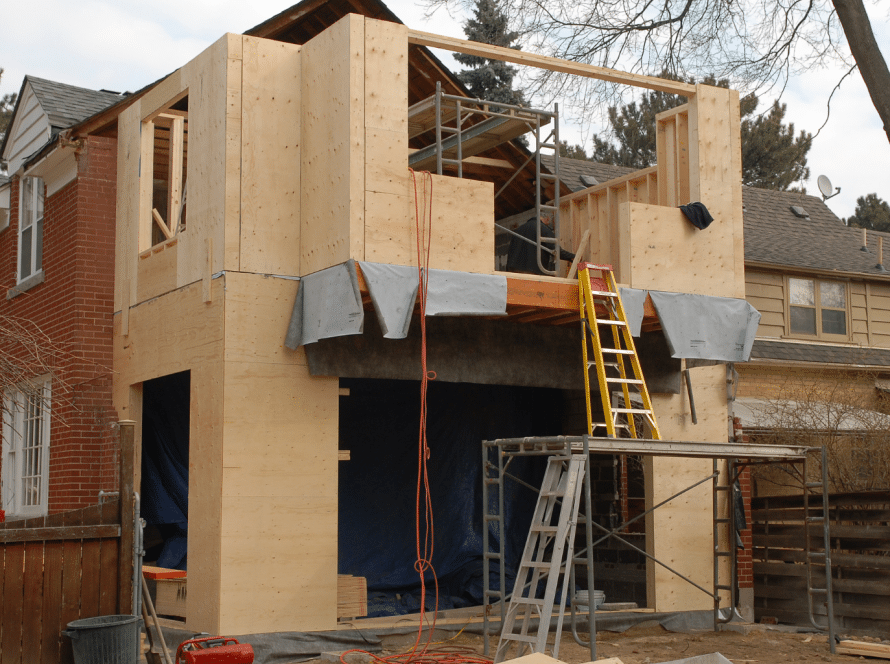

It is essential to first determine the cost of the home addition before looking for financing options. The cost that will be incurred at the end of the project depends on the kind of addition, materials used, and the project’s complexity.

Budget for Your Home Addition

First, decide how big and what kind of addition you will want. Do you wish to construct a single room or renovate the whole floor? Average home additions will range from $20,000 up to $100,000 or more depending on the size of the project.

What to Consider:

Design and Architecture: If the addition involves professional design or architectural drawings, then factor these costs into your budget.

Labor and Materials: Construction labor costs vary from place to place and also from the complexity of the project. Pricing can also be influenced by materials you wish to use, such as wood, steel, or concrete.

Permits and Fees: You may need building permits, which will increase the total cost of the project.

Review Your Financing Options

When you have a good idea of what your home addition will cost you, the next step is to look for financing options. Some of the most common sources of funding a home addition are discussed below.

Home Equity Loan

Home equity loan is a popular arrangement for homeowners who need to finance a home improvement project. It enables you to borrow against the equity you’ve accumulated on your home.

How It Works:

A home equity loan is a lump sum amount, which is repaid over a fixed term often with a fixed interest rate. It is a secured loan against your home, which means that if you default in paying the loan, your lender can take possession of your property.

Pros:

Lower Interest Rates: Home equity loans have lower interest rates than unsecured loans, or credit cards.

Tax Deductible: Interest on a home equity loan is deductible in taxes if the money borrowed is to be used for home improvement.

Cons:

Risk to Your Home: Because the loan is secured by your home, you can lose it if you fail to make your payments.

Limited Loan Amount: You can usually borrow up to 85% of the equity of your home; this may not be sufficient for larger additions.

HELOC– Home Equity Line of Credit

A Home Equity Line of Credit (HELOC) is like a home equity loan in that you’ll get a revolving line of credit rather than a lump sum. You may borrow from this line as you require, at an interest rate only on the amount you have used.

How It Works:

With a HELOC, the lender grants you a credit line, based on the equity you have in your home. During the draw period (usually five to ten years) you can borrow as much or as little as you want. After the draw period, you enter the repayment period which can take up to 20 years.

Pros:

Flexible Access to Funds: You can borrow and repay the funds whenever you need them, so it is perfect for projects that have fluctuating costs.

Lower Interest Rates: As with home equity loans, HELOCs generally come with lower interest rates than other loans.

Cons:

Variable Interest Rates: Many HELOCs are of a variable nature and, therefore, the interest rates may rise from time to time.

Risk to Your Home: Just like home equity loans, failure to pay back the amount borrowed can lead to foreclosure.

Personal Loan

A personal loan is an unsecured loan that you can spend on different things such as home additions. A personal loan, unlike home equity loans and HELOCs, does not require you to use your home as collateral.

How It Works:

Personal loans are usually issued at fixed terms and interests. Because of their unsecured nature, they usually attract a higher interest rate than home equity loans. But they might be a good choice if you don’t have much equity in your home, or if you do not want to put your property at risk.

Pros:

No Collateral Required: You don’t have to put your home as collateral which lessens the chance of losing your property.

Quick Approval: Personal loans tend to have faster approval times and can be obtained from several different lenders such as banks, credit unions, or online lenders.

Cons:

Higher Interest Rates: Personal loans are usually charged higher interest rates than secured loans.

Smaller Loan Amounts: Lenders provide smaller loans than a home equity loan or HELOC.

Cash-Out Refinance

A cash-out refinance will enable you to replace your old mortgage with a new mortgage of a higher value, and you get the difference in cash. This is another way of leveraging your home’s equity in order to finance a home addition.

How It Works:

With a cash-out refinance, you refinance your mortgage at an amount higher than what you owe, and you get the extra money to do your project. You’ll be left with a new mortgage balance with the amount you took for the home addition.

Pros:

Potential for Lower Interest Rates: You can access a lower interest rate than that of other loans.

Larger Loan Amount: A cash-out refinance provides a greater amount of financing than other loan options.

Cons:

Increased Monthly Payments: Because you’re refinancing your mortgage, your monthly amount would rise, especially if you’re taking out a significant amount.

Closing Costs: A cash-out refinance usually has closing costs that can vary but might be high.

Government-Backed Loans

Qualified persons can take government-backed loans such as an FHA 203(k) loan to finance home improvements and home additions. These loans are targeted at homeowners that do not have a lot of equity or need to finance their homes.

How It Works:

The FHA 203(k) loan enables you to take a loan to improve your home as part of your mortgage. It is a very good choice for homeowners who require assistance in financing both the purchase and renovation of their home.

Pros:

Lower Credit Requirements: FHA loans tend to have relaxed credit score requirements so they are available to many homeowners.

Inclusion of Renovation Costs: The cost of adding an addition to your home can be incorporated into the loan so it’s easy to handle the cost.

Cons:

Lengthy Approval Process: FHA 203(k) loans are slower to process than the traditional ones.

Additional Fees: These loans may require you to pay a higher fee or take insurance.